Table of Content

The policy may also offer up to $750 worth of coverage for your business property while it's away from your home. If not, there may be options to increase those coverage amounts with a homeowners policy endorsement. Operating a business is challenging enough without having to worry about suffering a significant financial loss due to unforeseen and unplanned circumstances. Small business insurance can protect your company from some of the more common losses experienced by business owners, such as property damage, business interruption, theft, liability, and employee injury. Depending on the risk profiles of you or your business, which may include creditworthiness, the insurer determines the compensation.

Here are three options to consider when insuring your homebased business. The commercial insurance content available on this page is for informational purposes only and not for the purpose of providing legal or financial advice. If you have any employees most states will require you to carry worker's compensation and unemployment insurance. Some states require you to insure yourself even if you are the only employee working in the business. A single lawsuit or settlement could bankrupt your business five times over.

(Junior/Senior) Business Analyst (m/w/d)

Home based businesses can range from small consulting practices to larger retail operations. These options can help serve the needs of any home based business in a cost-effective way. If one of your employees gets injured or sick due to a work occurrence, workers compensation insurance pays medical bills. Sole proprietors are often exempt from workers comp requirements, but if you have employees make sure you understand your state’s workers comp laws. If your accounts receivable records are lost due to a problem covered by the policy, this coverage reimburses you for the amounts you can’t collect from customers.

Standard home insurance has a $500 limit on business property that’s away from the residence premises. So if you’re using an expensive video camera away from home, coverage is limited. To decide if a home-based business insurance policy is worth considering, here are a few things to know. If you need higher reimbursement limits or you have additional coverage needs, you may want to look into getting an in-home business policy or buying a more robust business owners policy.

Business property endorsement

A personal auto insurance policy won’t cover business use of a vehicle. An endorsement to your home insurance policy will add extra coverage for a small operation out of a home. But larger businesses or professions that need specialized coverage may need a stand-alone business insurance policy. For low-probability, catastrophic losses, insurance is typically seen as beneficial by economists and consumer advocates in the United States, but not for high-probability, minor losses. Customers are urged to avoid ensuring failures that would not significantly interrupt their lives and to choose large deductibles. This is linked to less health coverage against low-probability losses being purchased, which might lead to increasing inefficiencies due to moral hazard.

We do not provide any form of advice if you call us to enquire about or purchase a product. HomeHQ by PolicySweet could provide coverage for businesses that operate from a mobile space like a kiosk or cart as long as business operations are primarily run from the location of a home. This could include businesses like a DJ, pet walking service, and coffee cart company. When deciding what type of policy to choose, consider the amount of financial risk you’re willing to shoulder, as one major loss could mean the end of your business. Still, some experts say an endorsement on a home insurance policy would be suitable for a small home business with minimal equipment and no business visitors or business deliveries to the home. For example, someone who telecommutes part-time using a home computer and fax might find an endorsement a reasonable option.

See What Our Customers Are Saying:

Most people believe that life insurance plans that pay interest are a type of riba , and some people even believe that policies that pay no interest are a form of gharar . Some claim that the actuarial science used in the underwriting proves gharar is not existent. Although some Jewish Torah scholars have highlighted concerns about insurance as a way to circumvent God's will, most think it is appropriate in moderation. When setting premiums and premium rate structures, insurance companies consider measurable criteria, including location, credit ratings, gender, employment, marital status, and educational level. Nevertheless, using such variables is sometimes viewed as unfair or illegally discriminatory. The response against this practice has occasionally resulted in political debates over how insurers decide prices and regulatory involvement to limit the factors employed.

An in-home business owner’s policy is a step up from a homeowners endorsement. It is essentially home insurance and a business policy rolled into a single policy designed specifically for home-based businesses, eliminating gaps and duplications in coverage. These policies offer coverage such as business liability and replacement of lost income, and homeowners coverages such as fire, theft and personal liability. You can increase protection from your homeowners policy by adding an endorsement, or rider, to it. This is the least expensive option for protecting your business assets, but it also offers the least coverage and could leave you with a great deal of risk. A typical endorsement can cost you as little as $25 per year and you can increase the policy limits from the standard $2,500 to $5,000.

Your home insurance policy’s personal property coverage will typically cover up to $2,500 in business property for on-premises business-related losses, and $250 to $500 for off-premises losses. Most standard homeowners insurance companies offer a policy endorsement to increase the limit of liability on property used for business purposes. This policy add-on will increase your business property coverage limits to $5,000 for on-premises losses and $1,000 for off-premises losses. Even those that cover some business loss expenses most likely don’t extend to liability for visiting customers or those who consume a product the business produces.

However, it typically doesn’t include liability protection related to business activities, and if the loss occurred in a detached structure on your property, your insurance claim would most likely be denied. Home business insurance is intended for a variety of businesses with different coverage needs. Insurers understand this, and will generally be able to write you a policy that fits your business or direct you to the correct additional coverage options. If you're a freelance web developer, you’ll have different insurance needs.

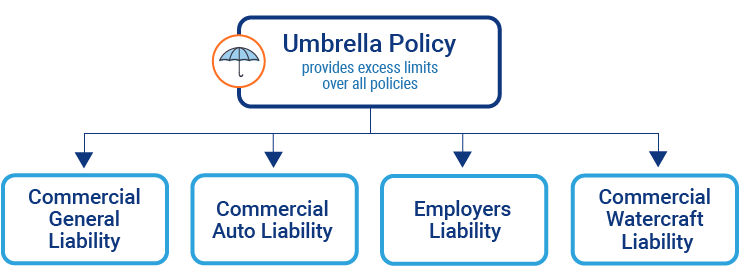

Home insurance companies typically offer endorsements that you can add to a homeowners policy to get more business coverage. An umbrella policy increases your liability limits beyond the amount in your underlying policy. One caveat to keep in mind — your umbrella coverage won’t supplement business losses that aren’t covered by your homeowners insurance. In order for your umbrella insurance to take effect for your business, you need to make sure the business-related loss is covered under an existing home business endorsement or policy. Should one of your employees become injured while on the job, your business insurance won’t compensate them for lost income. You’ll need to add workers compensation coverage to your business to protect your employees.

Meet with your State Farm® agent to discuss the insurance needs of your homebased business. Plan to have $5,000 or more worth of business property kept at your homebased business location. Plan to have less than $4,999 worth of business property kept at your homebased business location.

Your financial situation is unique and the products and services we review may not be right for your circumstances. We do not offer financial advice, advisory or brokerage services, nor do we recommend or advise individuals or to buy or sell particular stocks or securities. Performance information may have changed since the time of publication.

Juan is a travel enthusiast with 25 countries visited so far, Scuba diver and Bike rider, believes in working hard to enjoy life to the fullest. Tips to help you remove some risk from starting your small business. RLI has a listing of more than140 unique businesses that qualify for Home-based Business Insurance. The The National Association of Insurance Commissioners is the U.S. standard-setting and regulatory support organization. Through the NAIC, state insurance regulators establish standards and best practices, conduct peer review, and coordinate their regulatory oversight. There is more than $425 billion dollars in revenue generated by U.S. businesses each year.

No comments:

Post a Comment